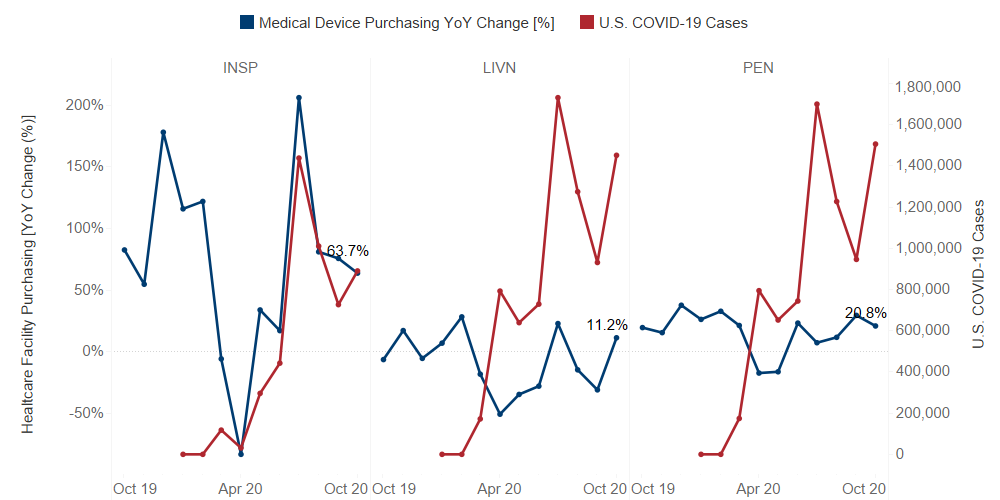

Since the onset of COVID-19, Guidepoint Qsight’s healthcare facilities purchasing dataset has been capturing the effects of the pandemic on several medical device manufacturers.

As expected, as U.S. COVID-19 cases rose, healthcare facility purchasing declined. While all manufacturers saw a dip in healthcare facility purchasing in April 2020, some companies were able to rebound better than others.

The Leaders:

Inspire Medical Systems (INSP): While Inspire was negatively impacted by COVID-19 in the first half of 2020, we observed strong growth in spending in the second half of the year. The rebound can be attributed to the resuming of procedures that backlogged because of the pandemic. Also, Inspire Medical Systems announced multiple coverage policies with various healthcare insurance providers, such as Cigna, Blue Cross Blue Shield, and Humana, increasing the number of patients and physicians that can have access to Inspire’s sleep apnea therapies.

Livanova (LIVN): According to Qsight’s healthcare facility purchasing dataset, Livanova’s total spend tracks closely with new U.S. COVID-19 cases due to the FDA’s authorization of Livanova’s Advanced Circulatory Support products for use in Extracorporeal Life Support to treat people with severe cases of COVID-19 in April 2020. Livanova’s other products, in both the cardiovascular neuromodulation businesses, saw a decline in healthcare facility purchasing related to the impact of COVID-19 on procedure volumes.

Penumbra (PEN): Penumbra’s year-over-year growth was positive during the second half of the year, seemingly unaffected by the rising case count of COVID-19 in the U.S. This is mainly due to Penumbra’s Indigo System for vascular thrombectomy as well as the unprecedented strong performance of the Lightning 12 system launch in July.

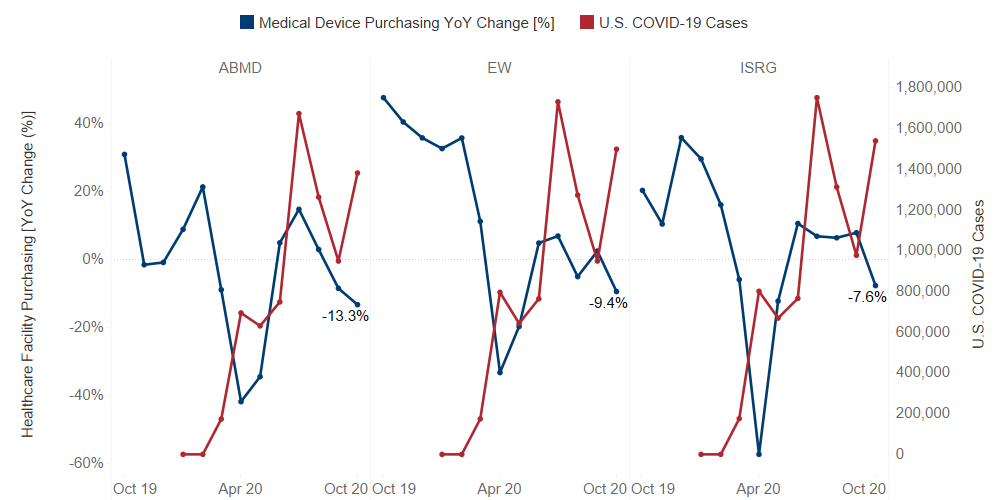

The Fighters:

Abiomed (ABMD): Despite Abiomed showcasing a positive year-over-year growth in June and July of 2020, our dataset indicates a steady decline in purchasing. In their earnings, management stated that High-Risk PCI (more elective) declined 8% in 3Q20, while cardiogenic shock (more emergent) increased 1%. The data implies that the resurgence of COVID-19 has put a pause on the recovery.

Edwards (EW): Focusing on TAVR, Edward’s significant year-over-year growth in 4Q19 set a difficult comparison for growth this year. With most of the backlogged procedures already worked through, Edwards must rely on new patient referrals, which are currently negatively impacted by the surge in new COVID-19 cases, as well as increased hospitalizations.

Intuitive Surgical (ISRG): Demand for robotic-assisted surgery has been growing in recent years, however, the COVID-19 pandemic has significantly disrupted Intuitive’s business. Our data is showing healthcare facility purchasing declines in October, which could be attributed to the increase in new U.S. COVID-19 cases. Additionally, the launch of the extended use instrument program, which increased the number of uses of many da Vinci instruments, reduced the price-per-use on core instruments but also caused a decrease in the number of sales.

Post created by: Shimul Sheth, Quantitative Analyst, Guidepoint Qsight