Guidepoint Qsight’s healthcare facilities purchasing dataset captures trends in multiple segments within the MedTech space. We break down insights on these segments and the top manufacturers in the space.

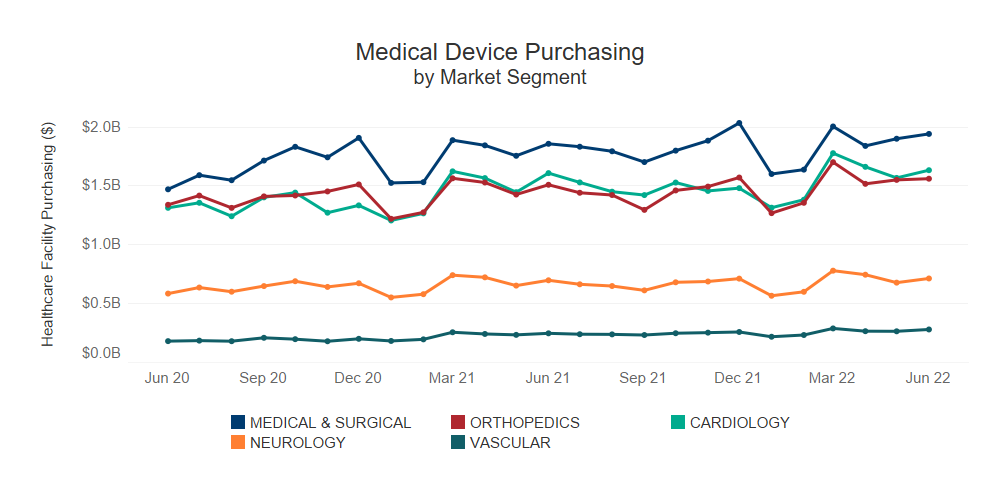

- Through the 2020 and 2021 winter COVID-19 surges, U.S. medical device purchasing decreased. This was particularly true in segments that rely on elective surgeries such as Medical & Surgical, Cardiology and Orthopedics. As COVID-19 cases increased, healthcare facilities faced staffing shortages, choosing to prioritize all non-elective procedures.

- As the US is entering into a ‘new normal’ with COVID-19, our healthcare facilities purchasing dataset shows that all five segments have trended upwards since June 2020.

When looking at specific manufacturers, the top three players have experienced the largest shifts in the overall MedTech market share:

- While Medtronic holds the leader position in the MedTech market space, it saw a drop of 1.1 points in market share in 2022 after experiencing continued supply chain issues since the beginning of the year.

- Despite supply change disruptions, Stryker is gaining market share with an increase of .6 points in 2022.

- Johnson & Johnson saw a decline in market share (-0.6 points) from 2021 to 2022.

The above is based on Qsight’s healthcare facilities purchasing dataset analyzing over $15B in annual spend from the top players in medical devices across a panel of 2200+ distinct healthcare facilities and hospitals.

Post Created by: Kimberlee Ales, Senior Quantitative Analyst, Guidepoint Qsight & Shimul Sheth, VP of Quantitative Research, Guidepoint Qsight