Non-invasive aesthetics continues to grow, but the era of uniform, high-velocity growth across treatments has passed. In its place is rising a more disciplined phase defined by category-specific momentum, evolving patient preferences, and a growing reliance on real-world performance data to guide decisions.

Recent industry data from Qsight shows that non-invasive aesthetics remains resilient, even as growth moderates from the exceptional levels seen in the early 2020s. Rather than signaling a slowdown in demand, this shift reflects a market that is maturing.

Success now depends less on rapid expansion and more on understanding which treatments, technologies, and patient segments are driving sustainable value. In this environment, data-driven insight has become essential, not just as a forecasting exercise but as a practical tool for navigating complexity.

Key Takeaways: Non-Invasive Aesthetic Treatments

- Non-invasive aesthetics continues to grow, but momentum is now category-specific rather than market-wide.

- Neurotoxins remain the primary driver of repeat visits and patient retention across non-invasive treatments.

- Skin rejuvenation growth is outperforming other categories, led by lower-cost, lower-downtime treatments such as mechanical microneedling.

- Regenerative skincare reflects rising premium demand, with higher spend per patient and rising adoption.

- Retention, treatment sequencing, and value per patient have become more important growth drivers than new patient volume.

Non-Invasive Growth Is Becoming More Selective

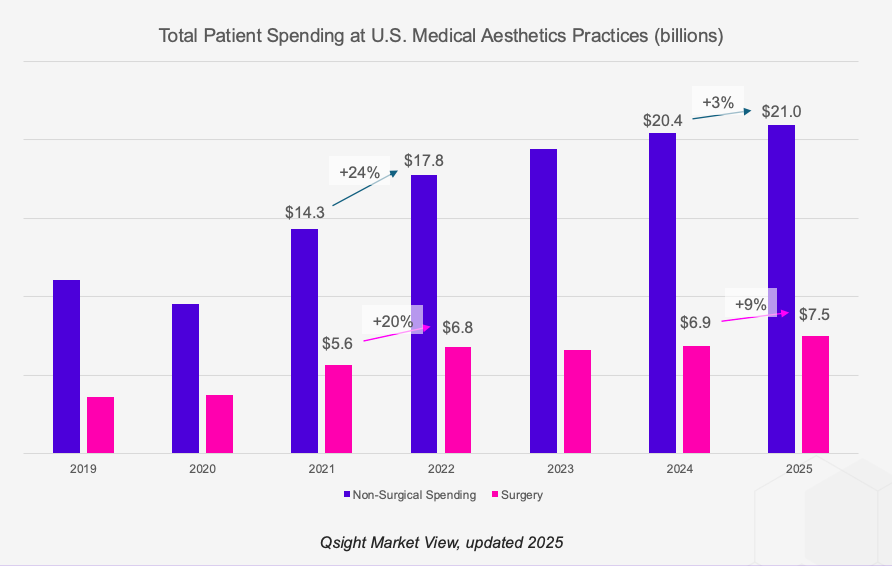

At the market level, medical aesthetics remains stable. According to Qsight data, total patient spending at U.S. medical aesthetics practices increased by approximately 4% year over year in 2025. For non-invasive treatments specifically, both average patient spend and overall patient retention rose by 2% YoY, suggesting healthy engagement.

Beneath that stability, however, performance varies widely by category. Some segments are expanding steadily, others are recalibrating, and a few are gaining share within otherwise flat or declining markets.

This divergence underscores a key reality for non-invasive aesthetics: growth is no longer evenly distributed. Treatments that align with patient expectations around cost, downtime, and outcomes are outperforming those that do not.

As a result, manufacturers and practices can no longer rely on category-level assumptions. Granular visibility into utilization, pricing, and patient behavior has become critical.

Neurotoxins Remain the Anchor of Non-Invasive Care

Among non-invasive treatments, neurotoxins continue to serve as the foundation of the aesthetics patient journey. They remain the most consistent driver of patient engagement and repeat visits, reinforcing their role as both an entry point and a long-term retention tool.

What has changed is the competitive landscape within the category. With more viable options like Daxxify and Letybo on the market, brands are increasingly relying on loyalty and rebate programs to influence reorder behavior and volume allocation at the practice level.

What makes this dynamic easy to miss is that category-level performance can appear steady even as share shifts underneath. For practices and manufacturers alike, data that reveals how patients move from neurotoxins into other treatments is increasingly valuable, particularly as patient retention becomes a primary growth driver.

Regenerative Treatments Are Recontouring the Filler Landscape

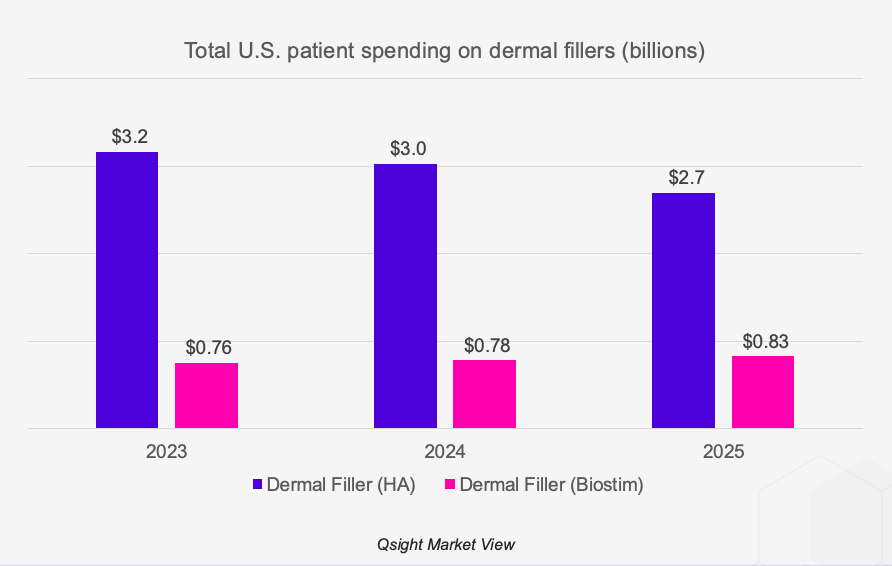

Dermal fillers remain a core non-invasive category, but performance within the segment is increasingly uneven.

Qsight data shows that in 2025, total hyaluronic acid filler spend had declined to $2.7 billion, down 11% YoY. This continues a trend of softening demand for traditional hyaluronic acid products that pharmaceutical providers are fighting to reverse. Over the same timeframe, however, biostimulatory injectables grew 6% to $830 million, capturing a growing portion of category spend.

This split suggests a reordering within the filler market, with patient dollars shifting toward treatments that offer collagen stimulation and gradual improvement.

Importantly, this means once-reliable filler treatment pairings are changing, too. It’s becoming less common to see patients receiving a dermal filler with a neurotoxin treatment in the same visit. For example, Qsight data shows that in Q3 2025, only 13% of neurotoxin patients received a filler in the same appointment, compared to 20% in early 2018.

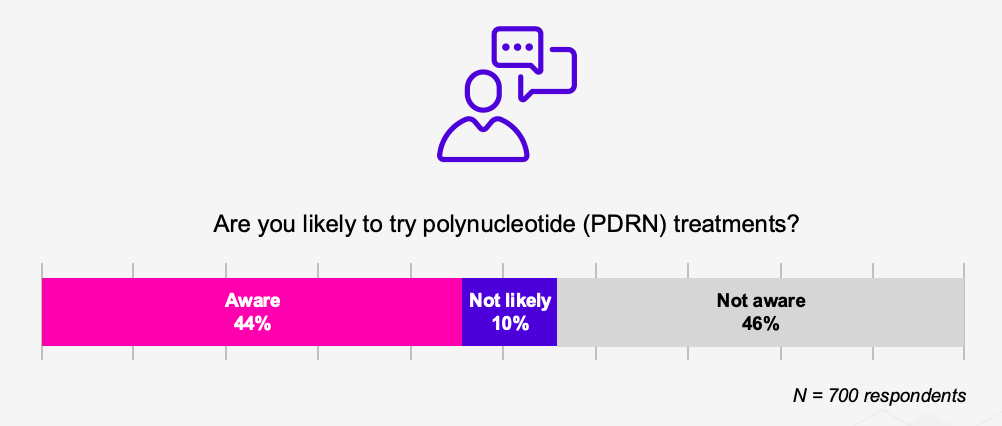

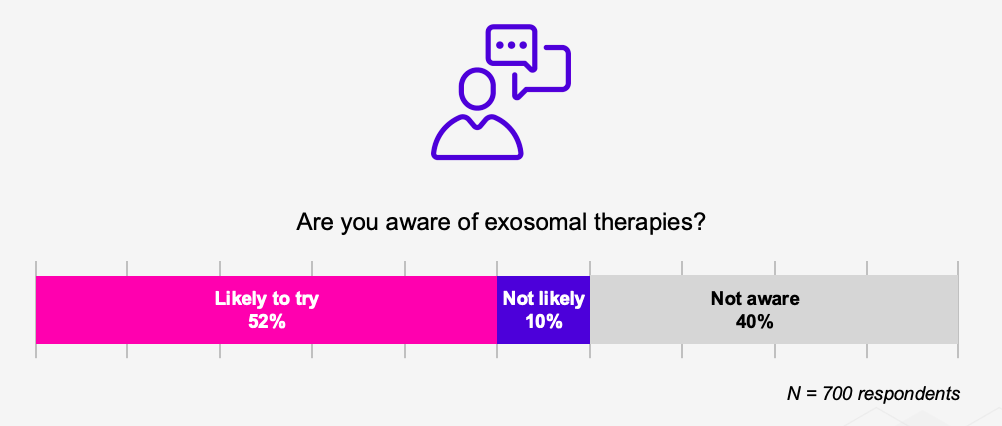

PDRN & Exosomes: A Signal of Premium Willingness

Regenerative treatment adoption remains measured—products and therapies like exosomes and PDRN are showing up in more practices, but they aren’t yet mass-market solutions. However, they certainly represent a segment to watch.

Their significance lies in what they reveal about patient behavior: a growing appetite for science-backed offerings that complement in-office treatments.

According to Qsight Consumer Tracker data, 60% of aesthetic patients are now aware of exosomal therapies, and 54% are aware of polynucleotides (PDRN). Most respondents who were aware of these therapies said they were “likely to try” them.

Source: Qsight Consumer Tracker

Energy-Based Devices Adjust to a Post–GLP-1 Landscape

Energy-based devices present a more complex picture. Overall spending has stabilized, but internal category shifts are reshaping performance. Skin-focused applications, including tightening and resurfacing, continue to attract patient interest, while non-surgical body contouring faces sustained pressure.

The rapid adoption of GLP-1 medications has altered patient priorities around weight loss, creating a competitive dynamic that device manufacturers must now account for. Rather than driving incremental growth, GLP-1s have introduced a recalibration period—one that rewards practices capable of repositioning treatments and setting realistic expectations.

Here again, data plays a critical role. Understanding how patient spend reallocates across categories is essential for informed product strategy and sales planning.

Non-EBD Skin Rejuvenation Is Gaining Strategic Importance

One of the clearest examples of performance-driven innovation can be seen in skin rejuvenation. Non-energy-based treatments have emerged as a standout growth area, driven not by novelty, but by accessibility.

Mechanical microneedling, in particular, has gained traction, likely due to its lower price point, minimal downtime, and broad range of clinical applications. Its 33% surge in growth has been further supported by compatibility with emerging skincare therapies, allowing practices to pair procedures with complementary products and protocols.

This pattern suggests treatments that integrate easily into existing workflows and patient routines could be seeing stronger adoption than those that introduce friction. Innovation, in this context, is less about new technology and more about fit.

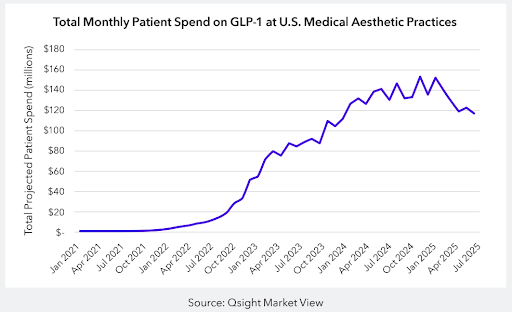

Weight Loss Has Become a Structural Entry Point

Weight loss and dietary lifestyle treatments remain a defining force within non-surgical aesthetics, despite significant recalibration after the official end of FDA-recognized shortages for semaglutide and tirzepatide.

Overall category growth has slowed down from earlier peaks, showing a decline for the first time in years. With $2.2 billion in total patient spending on weight loss and dietary/lifestyle treatments—roughly the same as the previous year—2025 marked the first time that this category didn’t see double- or triple-digit growth since the introduction of GLP-1s in 2021.

But GLP-1s have remained a key driver of medical aesthetics revenue despite shortages and regulatory pressures. Total quarterly patient spending on weight loss is still 10x what it was in 2021, and as a category, it represents the 2nd-highest patient retention rate, second only to neurotoxins. From 2024 to 2025, 46% of medical aesthetics patients returned for more weight loss treatments.

Weight loss is a category in flux, but there is promise and opportunity for brands, practices, and investors with the knowledge and tools to follow the data.

How Qsight Brings Clarity to a Fragmenting Market

Clarity depends on seeing the market from multiple angles at once. Qsight brings those views together through complementary data sets that reflect what is happening at the point of care, how practices are responding, and how demand is taking shape online.

- Market View provides near-real-time visibility into total market size and share by treatment type.

- Sales Measurement captures transaction-level behavior, revealing how patients allocate spend across procedures and products.

- Practitioner Tracker adds longitudinal insight into adoption patterns and how practices are adjusting their offerings over time.

- Social Intelligence captures activity across practice and practitioner influencer social channels, revealing which treatments and brands are gaining visibility and traction in the digital conversation.

Looking Ahead: Visibility Matters More Now Than Ever

The next phase of non-invasive aesthetics will reward precision. Treatments that fit naturally into ongoing care patterns and deliver consistent value are already absorbing a greater share of patient spend, while others continue to fade quietly.

As patient expectations continue to evolve, the organizations that succeed will be those that understand not just where the market is growing, but why. In a landscape shaped by shifting category leadership and changing behavior, data-driven insight is no longer optional. It is the foundation for navigating what comes next.

See What the Market Is Actually Doing: Request a Demo

If your decisions depend on understanding what’s strengthening, what’s slipping, and what’s coming next, request a demo today.