The AFib ablation catheter market has more than tripled in size since 2018, and spending over the same time period has swelled almost 280%. The growth has been steady, and for years, the competitive landscape within it was relatively stable—that is, until pulsed field ablation arrived.

Pulsed field ablation (PFA) didn’t register in U.S. healthcare facility purchasing records until April 2023. Just three years later, it accounted for nearly 80% of AFib ablation catheter spend.

What follows is a map of that trajectory. We’ll cover how fast the change happened, what it did to legacy modalities, and how the competitive landscape within PFA has already started to reshape itself.

All data is drawn from Qsight Market Models: a MedTech market intelligence platform featuring purchasing data across more than 4,500 U.S. healthcare facilities.

Key Takeaways: The Pulsed Field Ablation Market in 2026

- Total AFib ablation catheter spend grew from roughly $1 billion in 2018 to $3.8 billion in 2025, with unit volumes rising from approximately 76,000 to nearly 250,000 over the same period.

- Pulsed field ablation went from zero presence in U.S. purchasing data in early 2023 to 78% of AFib ablation catheter spend by early 2026.

- RF ablation, the clear standard of care from 2018-2023, fell from 63% of spend in 2023 to 22% by the end of 2025.

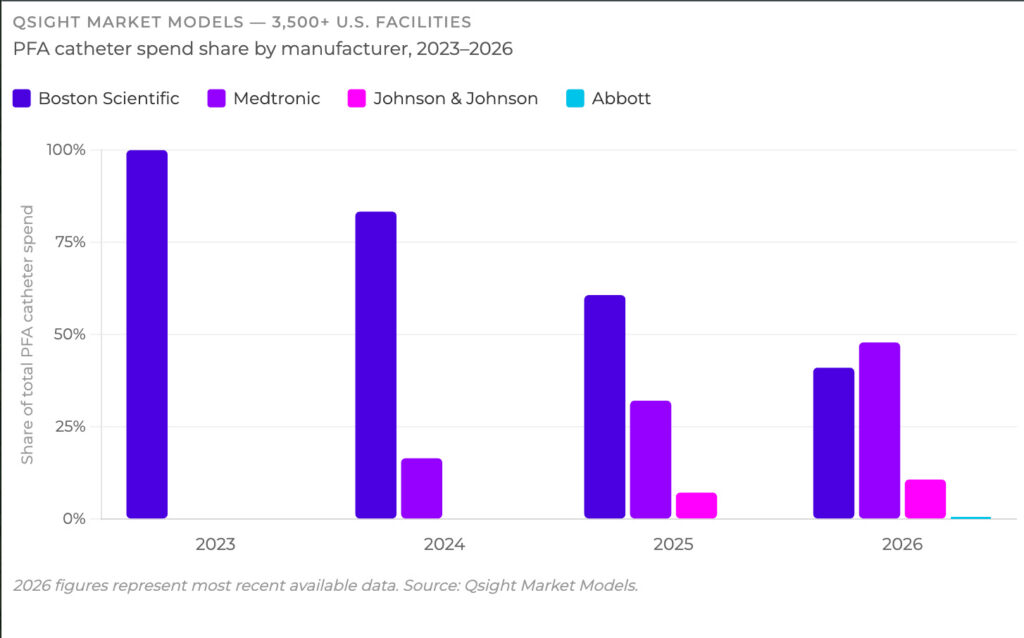

- Boston Scientific held 100% of PFA spend in 2023, but by early 2026, that share had declined to 41% as Medtronic, Johnson & Johnson, and Abbott entered the market.

- Total catheter unit volumes continued to grow at 20% year-over-year in 2025, even as the modality mix shifted dramatically toward PFA

Eight Years of Growth in the AFib Ablation Market

The AFib ablation catheter market has grown consistently for nearly a decade. According to Qsight Market Models, total catheter units rose from approximately 76,000 in 2018 to nearly 250,000 in 2025. Total market spend climbed from roughly $1 billion to $3.8 billion over the same period.

Year-over-year unit growth has held in the 20–25% range every year since 2019, excepting 2020. That kind of sustained volume growth reflects durable underlying procedural demand, rather than a category spike driven by a single product cycle.

The driver is well-documented. The prevalence of atrial fibrillation is rising globally, particularly among aging populations, and clinical guidelines have begun recommending catheter ablation earlier in the treatment pathway for select patients rather than defaulting to antiarrhythmic drug therapy as a first-line approach.

How a Stable Market Gave Way to New Ablation Techniques

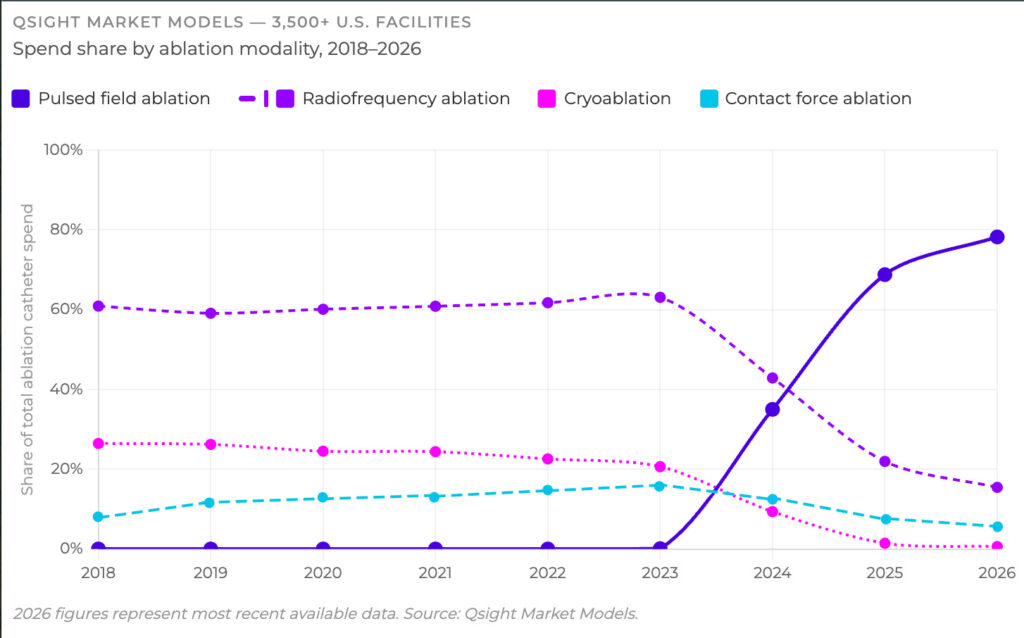

For the five years between 2018 and 2023, the AFib ablation catheter market was structurally consistent. Radiofrequency (RF) ablation held roughly 61% of spend and 67% of units throughout that period, making it the clear standard of care. Cryoablation maintained a steady 20–26% share of spend. Contact force ablation grew gradually, moving from 8% to about 15% of spend over the same window.

These shares barely moved year to year. For MedTech manufacturers, investors, and commercial teams tracking the category, the competitive landscape was predictable in a way that most device markets aren’t.

That changed in April 2023, when Boston Scientific’s FARAWAVE became the first pulsed field ablation catheter to appear in U.S. purchasing data.

How Fast the Pulsed Field Ablation Market Moved

Pulsed field ablation uses short bursts of electrical energy to create precise lesions in cardiac tissue without the thermal effects that characterize RF and cryoablation. Because the mechanism is non-thermal, it reduces the risk of damage to surrounding structures, a feature that has driven rapid uptake among electrophysiologists.

The speed of adoption in purchasing data has been notable. PFA accounted for roughly 35% of total ablation catheter spend in 2024, its first full year on the market. By 2025, that share had risen to 69%. In early 2026, it stood at 78%.

Unit share tells a complementary story: PFA moved from approximately 21% of catheter units in 2024 to 48% in 2025 and 57% in early 2026. The fact that both spend share and unit share are growing together confirms that this is real procedural volume, not a pricing effect.

Understanding the Gap Between Spend & Unit Shares

PFA’s spend share has consistently outpaced its unit share since entering the market: 35% of spend versus 21% of units in 2024, and 69% of spend versus 48% of units in 2025. That difference suggests PFA catheters carry a higher average selling price than the legacy modalities they’re displacing.

But it has been narrowing year over year, suggesting volume adoption is accelerating relative to the price premium. Manufacturers and commercial teams tracking competitive positioning in this category would do well to keep an eye on this trajectory.

What Happened to RF and Cryoablation

The effect on legacy catheter treatments has been sharp. RF ablation fell from 63% of spend in 2023 to 42% in 2024, then to 22% in 2025. Cryoablation went from 21% of spend in 2023 to under 2% by 2025. Contact force ablation, which had been on a steady upward trajectory for years, dropped from 15% to under 8%.

Both RF and cryo manufacturers are losing share in a market that is still growing in total units, which means the volume shift to PFA is outpacing whatever underlying procedural growth those modalities might otherwise have captured.

The Race Within the Pulsed Field Ablation Market

Boston Scientific’s first-mover advantage was significant. The company held 100% of PFA spend in 2023 and approximately 83% through 2024. But the competition within PFA has ramped up quickly.

Medtronic entered with PulseSelect in January 2024, followed by Boston Scientific’s next-generation FARAPOINT in February 2024 and FARAWAVE NAV in August 2024. Medtronic added Sphere-9 in November 2024, Johnson & Johnson’s Biosense Webster division launched Varipulse in December 2024, and Abbott entered with Volt in January 2026.

By early 2026, Boston Scientific’s PFA spend share had declined to 41%, while Medtronic had grown to 48%. Johnson & Johnson reached 11% of PFA spend after launching late in 2024, and Abbott’s Volt has already captured ~1% in its first months on the market.

Boston Scientific’s Position in Context

Though the share decline is meaningful, it’s happening in a rapidly expanding market. Boston Scientific’s absolute PFA revenue has continued to grow even as its percentage of the category has fallen, because the overall PFA market has expanded so significantly.

The competitive question going forward is whether new entrants will continue to erode Boston Scientific’s lead or whether the market will stabilize around current shares.

The Next Generation Is Already Here

Product launches within PFA have also reshaped the competitive picture at the brand level. Within Boston Scientific’s portfolio, FARAWAVE NAV has nearly displaced the original FARAWAVE: it held 32% of total PFA spend in early 2026, compared to just 9% for the original system.

Medtronic’s Sphere-9, which launched less than a year after the market-entry PulseSelect, already accounts for 46% of Medtronic’s PFA spend. The pace of within-portfolio turnover appears, at this stage, to be as fast as the broader modality change.

An Open Question About AFib Ablation Market Share

Total catheter units reached nearly 250,000 in 2025, up 20% year-over-year and consistent with growth rates since 2021. That sustained volume growth raises a question: is PFA cannibalizing existing RF and cryo procedures, or is it also expanding the addressable patient population for ablation?

The Medicare reimbursement landscape suggests expansion is plausible. Effective January 1, 2026, CMS added cardiac catheter ablation to its ASC-covered procedures list for the first time, a change analysts expect to expand both geographic access and overall procedure volumes by bringing ablation to lower-cost outpatient settings.

Whether those tailwinds are already reflected in the unit growth figures, or whether that expansion is still ahead, is the more consequential strategic question as the category matures.

MedTech Market Intelligence: Tracking a Market in Transition

The AFib ablation story is instructive beyond the electrophysiology market. A category that held its competitive structure for five years inverted completely in under three, with a second race starting within PFA before the first one is settled.

The open question about market expansion versus cannibalization, now complicated further by the CMS reimbursement change effective January 2026, means the most consequential data for manufacturers and commercial teams is still being written. Tracking it in near real-time, rather than waiting for quarterly earnings or annual projections, is where purchasing data earns its place.

Request a Demo Today

Qsight Market Models covers the MedTech sector across 4,500+ U.S. facilities, updated monthly. Request a demo to see what the data shows for your market’s dynamics.