Gen Z is leading a generational shift in the medical aesthetics market. For this rising cohort, preventive aesthetic treatments are a key part of how they define wellness. That means procedures like injectables and laser resurfacing aren’t exclusively about reversing aging anymore.

Once viewed as luxury splurges for middle-aged consumers, aesthetic treatments are increasingly being seen as routine self-care by younger generations. This marks a major departure from the traditional lifecycle of aesthetic medicine.

Here, we’ll take a closer look at this shift and what it means for aesthetic brands and manufacturers.

Key Takeaways: Gen Z Preventive Aesthetics

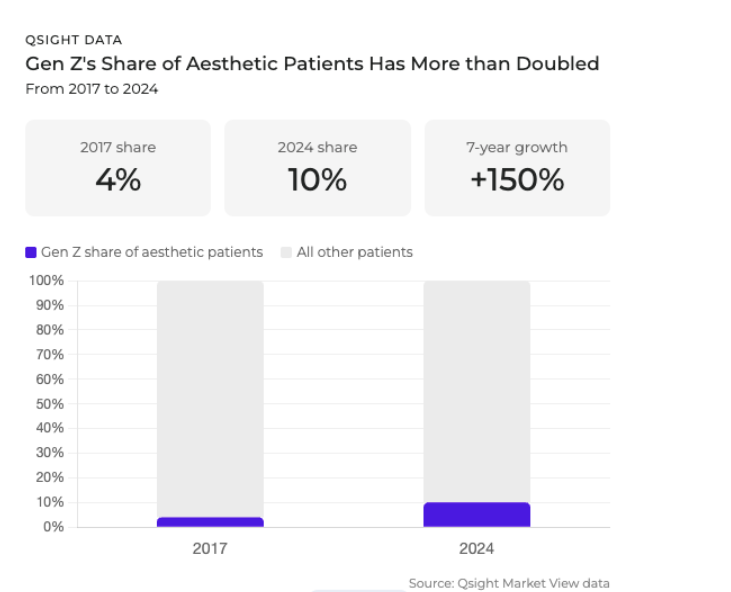

- Gen Z’s share of the aesthetics patient population grew from 4% in 2017 to 10% in 2024, according to Qsight data.

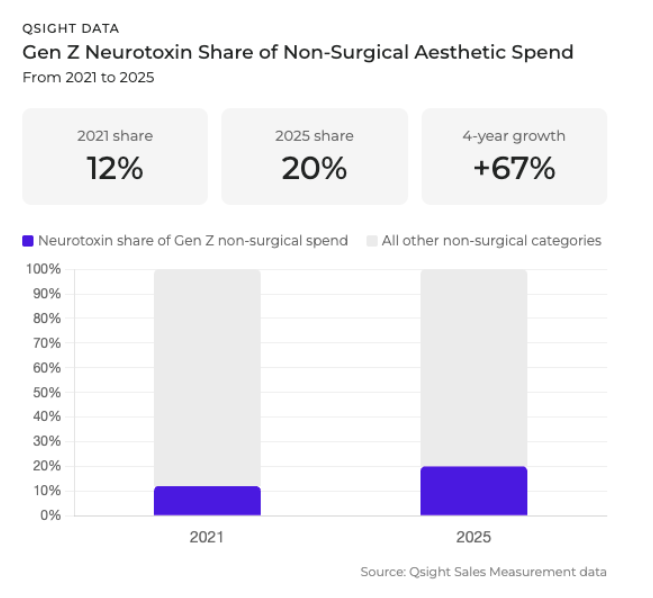

- Neurotoxin spending rose from 12% of Gen Z’s total non-surgical aesthetic spend in 2021 to 20% in 2025, per Qsight Sales Measurement data.

- The Gen Z “prejuvenation” mindset spans neurotoxins, medical-grade skincare, collagen-stimulating treatments, skin resurfacing, and more.

- Younger patients are entering the aesthetics market earlier and with more intention, treating non-invasive cosmetic procedures as long-term investments rather than one-off corrections.

- Brands that track Gen Z demand at the cohort level (by treatment, channel, and geography) are better positioned to meet rising demand where it’s actually concentrated.

Prejuvenation Replaces Restoration in Aesthetic Medicine

In years past, patients typically entered the aesthetic world in their 40s or later, often with a specific concern to correct. Gen Z is flipping that script. They’re stepping in earlier, not because something’s wrong, but because they want to maintain—or even optimize—what they already have.

This philosophy, often described as prejuvenation, is driving real behavior change. Consumers in their 20s are booking appointments for neurotoxins like Botox®, investing in skincare, and asking about resurfacing options as preventive choices tied to their sense of long-term health.

While “wellness” has definitions ranging from better sleep to more mindfulness, for Gen Z, “better appearance” is a top-three wellness concern.

What Prejuvenation Trends Actually Look Like in Practice

What the industry has started calling “tweakments”—subtle, low-downtime procedures applied early and maintained regularly—is the practical expression of the prejuvenation philosophy. Gen Z patients are engaging with a broad range of minimally invasive and non-invasive cosmetic procedures as part of an ongoing skin health strategy.

That includes:

- Neurotoxins (Botox, Dysport®) targeting early expression lines and fine lines before they set in

- Collagen-stimulating treatments like microneedling and biostimulatory injectables that build structural skin quality over time

- Skin resurfacing procedures, including chemical peels and laser treatments, used proactively to address skin texture, acne scars, and early sun damage

- Professional-grade skincare formulations with growth factors, peptides, and hyaluronic acid that extend the results of in-office treatments at home

- Hyaluronic acid fillers, used conservatively for subtle volume and hydration—a different application than the correction-focused approach common among older cohorts.

The Gen Z Non-Surgical Treatment Mix: Beyond Botox

The neurotoxin story gets the most attention, but it’s only part of what’s driving Gen Z’s growing footprint in the medical aesthetics market. A broader range of non-invasive cosmetic procedures is part of how younger patients approach preventive aesthetics, including dermal fillers, laser skin rejuvenation, chemical peels, and medical-grade skincare routines.

Neurotoxins: Botox and Dysport Lead Entry and Spend

Qsight data shows that among Gen Z patients entering aesthetic practices for the first time, neurotoxins are the dominant category. At the individual treatment level, Botox ranks first among first-time procedures, with Dysport also appearing in the top five, per Qsight Sales Measurement data. By total dollars spent on an ongoing basis, Botox holds the top position across the cohort.

The application among younger patients skews preventive, targeting early expression lines and fine lines before they set, rather than correcting established wrinkles. This is the “Baby Botox” paradigm in practice: lower doses, earlier start, longer-term maintenance cadence.

Collagen-Stimulating Treatments and Skin Quality Procedures

Qsight data shows microneedling gaining popularity across the market. This makes sense for younger patients focused on skin texture, skin firmness, and collagen density: all outcomes that align with the preventive logic Gen Z applies to aesthetics broadly. These treatments don’t deliver instant transformation but rather build cumulative skin quality improvement over time, which fits nicely with the long-term investment mindset.

Chemical peels and other skin resurfacing procedures occupy similar territory. Used proactively, they address early sun damage and uneven skin texture before these concerns become more entrenched. For Gen Z patients who started skincare early and are now looking to extend those results in-office, resurfacing is a natural next step.

Dermal Fillers in a Preventive Context

Among younger patients, hyaluronic acid filler use tends toward the conservative end, focused on maintaining hydration and subtle structure rather than restoring volume that hasn’t yet been lost. Though fillers have faced some headwinds—a 7% decline in sales in 2025, pop stars like Charli XCX publicly claiming fillers are “over”—there’s still confidence in this segment’s staying power.

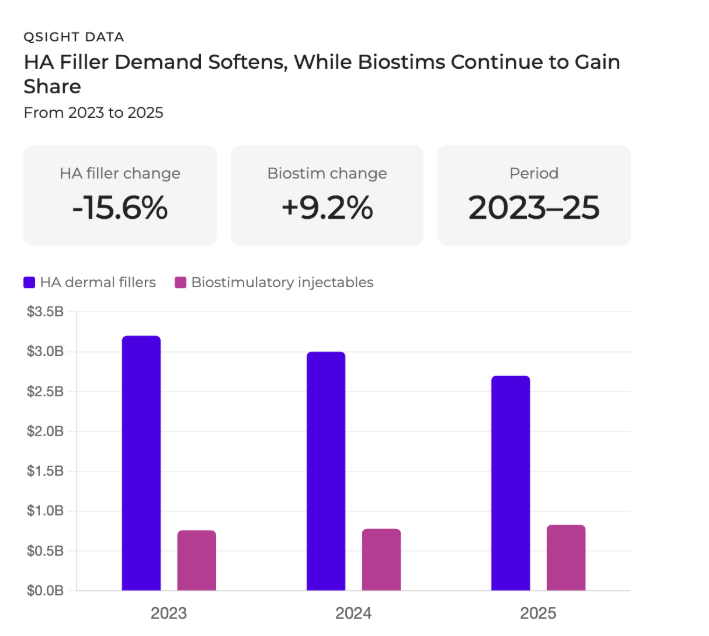

That’s especially true as biostimulatory fillers appear to be gaining the share that traditional HA fillers are losing. Total U.S. patient spending on HA-based dermal fillers declined 15.6% between 2023 and 2025, dropping from $3.2 billion to $2.7 billion, per Qsight data. Over the same period, biostimulatory injectables grew 9.2%, from $760 million to $830 million.

Real-Time Data Shows Generational Growth in the Aesthetics Market

Qsight data shows that in 2017, Gen Z made up just 4% of all aesthetics patients. By 202, their share had grown to 10%. This growth signals not only a demographic aging into eligibility but also early engagement with aesthetics across multiple non-surgical categories, including neurotoxins and professional-grade skincare.

Preventive Botox Is No Longer Niche

One of the clearest signs of Gen Z’s mindset around aesthetics is their early and intentional use of neurotoxins as part of a long-term care strategy.

Qsight Sales Measurement data shows that in 2025, neurotoxin treatments made up 20% of Gen Z’s total non-surgical aesthetic spend, up from 12% in 2021. That level of growth reflects a generational realignment in when and why patients begin aesthetic treatments.

For brands and practices, this creates an opportunity to meet early-stage patients with education, appropriately scaled treatment plans, and messaging that emphasizes continuity and confidence rather than correction.

Personalized Treatments: Skincare as a Sustained Revenue Channel

Qsight Sales Measurement data shows that Gen Z patients are contributing to steady growth in professional-grade skincare. For this cohort, skincare isn’t typically the entry point into aesthetics (neurotoxins hold that position). But medical-grade skincare functions as a durable component to in-office treatments, extending results between visits and representing a consistent spending category across the patient lifecycle.

Hydrafacial is a notable example. It ranks among the top five most common ongoing services for Gen Z patients by both visit frequency and dollars spent, per Qsight Sales Measurement data. Its position in the treatment mix reflects how younger patients blend skin health maintenance with in-office care, returning regularly for a service that sits at the intersection of clinical skincare and aesthetic treatment.

For companies operating in the skincare space, segment-specific tracking offers ways to capitalize on that sustained footprint. Qsight’s basket analysis and patient demographic data allow brands to track how skincare and injectable categories interact across age groups and spending patterns. This shows not only what’s selling but also who’s buying it, and how that aligns with overall treatment behavior

How Gen Z Compares to Older Cohorts

The contrast with older patient cohorts is instructive. Millennials, Gen X, and Boomer patients historically entered aesthetics later, often through plastic surgeons or dermatologists, and frequently with a corrective goal, such as addressing volume loss, deep wrinkles, or laxity. Surgical options like facelifts remained relevant for patients whose concerns had moved beyond what non-invasive cosmetic procedures could address.

Gen Z is building a different relationship with aesthetics clinics from the start. By engaging with minimally invasive procedures earlier, they’re aiming to delay or reduce the need for more significant intervention later. Whether that plays out as intended over time remains to be seen—but the intent is driving real spending behavior now.

Medical Aesthetics Market Intelligence: Understanding the Gen Z Patient Lifecycle

The combination of early engagement with neurotoxins and skincare suggests new lifecycle dynamics. Qsight tools give brands and providers the visibility to monitor emerging patterns across patient age groups.

With Qsight, brands can track:

- Treatment frequency by cohort

- Product bundling trends across service lines

- Shifts in average spend per visit for younger cohorts

- Changes in patient acquisition across medspas and physician practices

These insights help teams anticipate where Gen Z is headed and how to stay ahead of it.

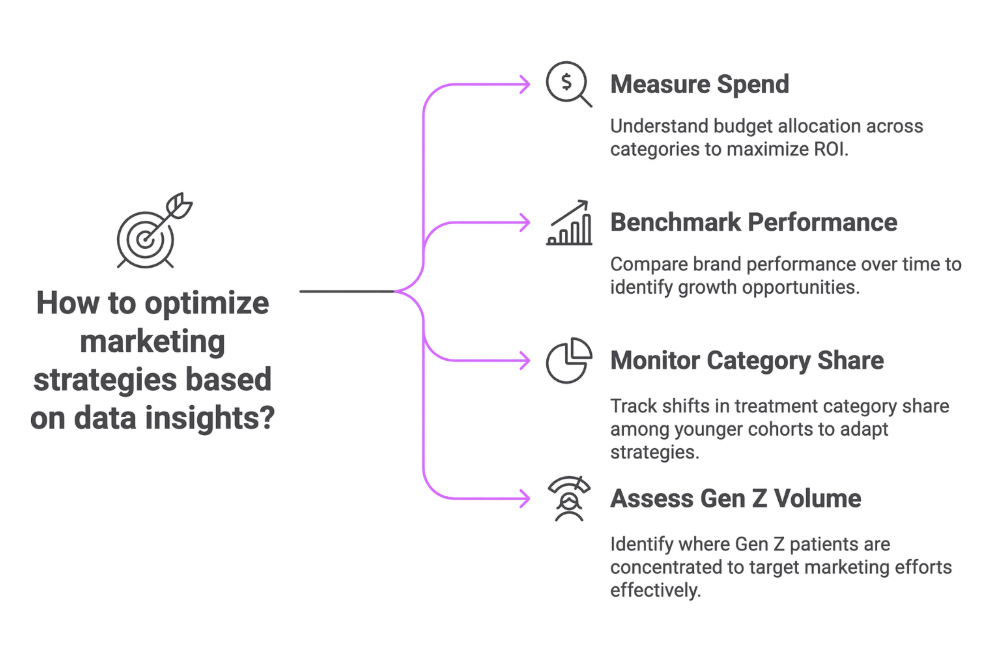

Strategic Considerations for Brands and Providers

Qsight’s tools allow teams to move from anecdotal decision-making to data-driven strategy. With this product suite, companies can:

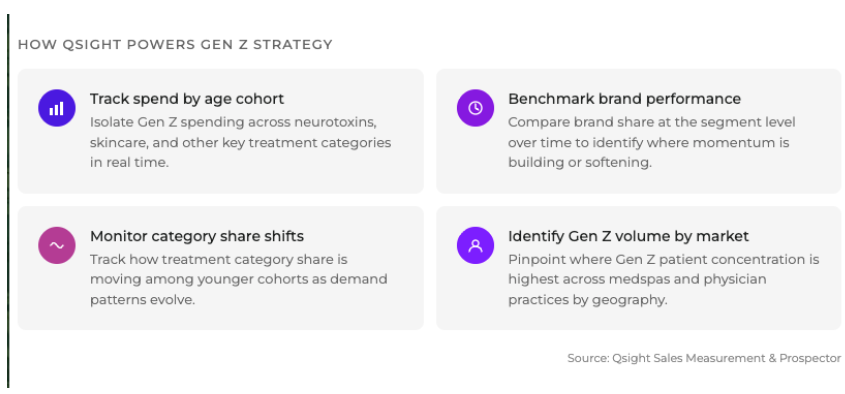

- Track spend by patient age across neurotoxins, skincare, and other key categories

- Benchmark brand performance at the segment level over time

- Monitor how treatment category share is shifting among younger cohorts

- Identify where Gen Z patient volume is concentrated across medspas and physician practices by geography

Qsight’s ability to isolate spend by age cohort, alongside pricing, practice type, and procedure data, gives brands a more accurate picture of where, and with whom, momentum is building.

Looking Ahead: The Gen Z Standard

Gen Z isn’t retracing Millennial footsteps. They’re taking a different path: one that’s earlier, more integrated, and deeply intentional. They’re not hesitant about injectables or medical skincare. What’s more, they’re informed, proactive, and investing in aesthetic care as part of a broader commitment to wellness.

With that comes a new set of expectations: how treatments are framed, how services are delivered, and how brands communicate. The future of medical aesthetics belongs to those who understand the people shaping demand. Right now, that’s Gen Z. And the opportunity to meet them with precision is here.

Understanding these patterns is critical for planning. Companies aiming to engage younger patients can use this data to guide decisions around:

- Product mix optimization by practice channel

- Brand share performance in Gen Z–dense markets

- Generational trends in category growth

Qsight’s ability to isolate spend by age cohort, alongside pricing, practice type, and procedure data, gives brands a more accurate picture of where, and with whom, momentum is building.

Get Aesthetics Consumer Behavior Data Tailored to Your Market. Request a Demo.

Want to track how Gen Z is spending by treatment, brand, and visit? Explore how Qsight’s real-time data tools can help your team plan with confidence. Request a demo today to get started.